Market sentiment: "Burying correction dreams"

Many professional bears have given up and are now sitting on the long side. The situation is different for private investors, who are more likely to be out. The bottom line is that this is taking strength out of the market.

Summary

The slump expected by many professionals at the beginning of the year as a result of the final rally failed to materialize, driving 12% into equities and out of short positions. The sentiment index for this group fell to -11 points. The situation is quite different for private investors, 10% of whom have sold shares and for the most part moved to the sidelines. According to Joachim Goldberg, there is a clear risk aversion among the latter.

The behavioral economist now sees less potential support from buyers on the downside and hardly any fodder for a squeeze on the upside. But even if the DAX looks a little battered on balance with today's survey, it is not so much the local investors who will determine the coming days. There is a lack of long-term capital from abroad for "more momentum".

10 January 2024. FRANKFURT (Goldberg & Goldberg). So far it has failed to materialize, the major setback that so many stock market players were counting on at the beginning of the year. Nevertheless, there has been a small downward correction of just under 1.8% since our last sentiment survey, although the DAX has almost made up for this by the time of today's survey. At the end of the day, a minus of 0.3% remains.

In view of the impressive DAX performance of the last two months of last year, there may well have been good arguments in many quarters for betting on a proper technical correction in January. Not only because historical statistics may speak in favor of such a development, but also because many assume that the US Federal Reserve is not in as much of a hurry to cut interest rates as the bond markets there have recently priced in. Opinions between central bank representatives and the market regarding the expected number of interest rate cuts also differ significantly. In short, overheated bond and equity markets should, according to popular opinion, cool down considerably. Or should they? If you listened closely, every day that the hoped-for stock market correction failed to materialize, you could also hear new arguments for further falling bond yields in the USA and the accompanying record-breaking rise in share prices.

At least with gains behind them

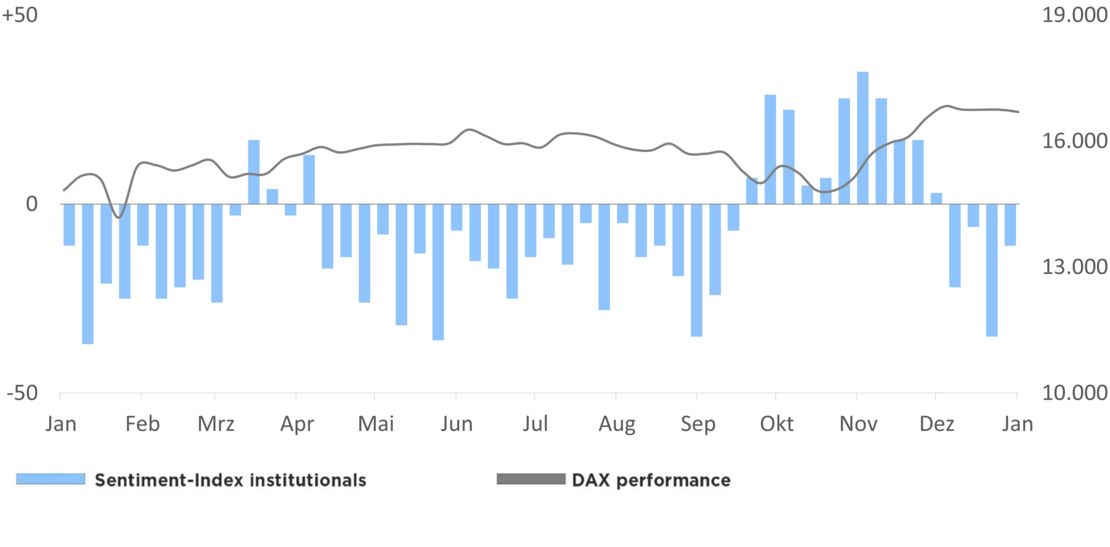

Sentiment among the institutional investors we surveyed with a medium-term trading horizon has now also improved significantly compared to the first extremely negative survey of the new year. Our Börse Frankfurt Sentiment Index rose by 24 points to a new level of -11. As we suspected, the majority of investors were probably not betting on a turnaround in the DAX, but were merely looking for a quick profit from setbacks in the first few days of January. This is supported by the fact that 12% of all respondents moved directly from the bear side to the bull side, i.e. turned their investments around 180° with a presumably decent profit.

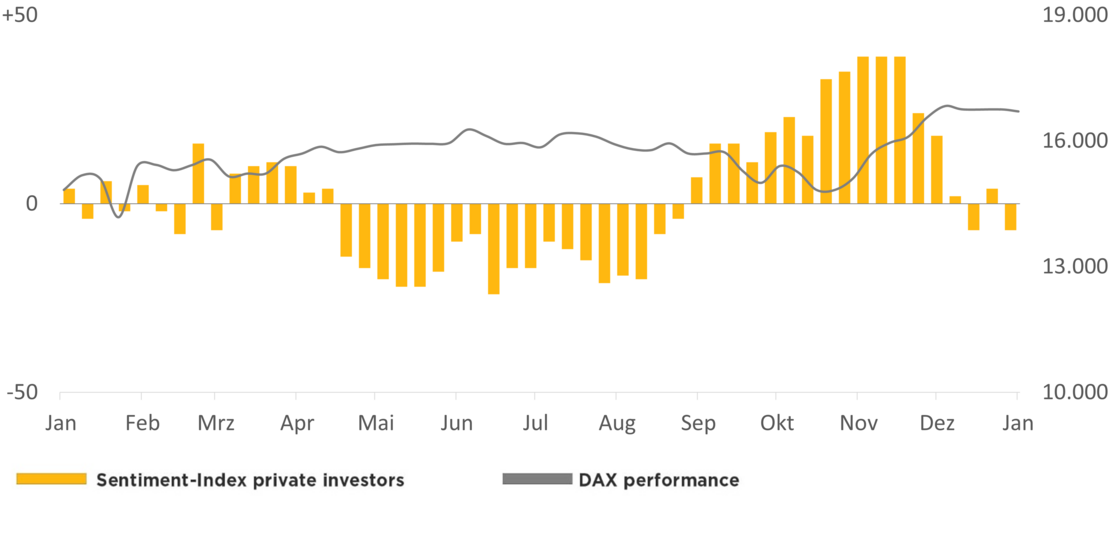

Among private investors, sentiment went in the opposite direction. The Börse Frankfurt Sentiment Index in this panel fell by 11 points compared to the previous week to a new level of -7. The bull camp fell by 10 percentage points, with almost all former optimists joining the neutral players on the sidelines. This is remarkable because since our last survey, there has hardly been an opportunity to sell shares at a significantly higher level than the index level at that time.

Risk-averse private investors

With today's survey, the strong sentiment gap between private investors and institutional market participants has narrowed significantly again. For the latter in particular, there is not much left of the strong pessimism of the previous week. It is also questionable whether the remaining short positions of domestic investors are large enough to provide sufficient supportive demand in the event of renewed DAX weakness at a lower level. Let alone trigger a significant squeeze on the upside if prices continue to rise.

Even if the DAX looks somewhat battered on balance with today's survey, it is less likely to be domestic positioning that will cause volatility over the next few days. Rather, the stock market barometer is dependent on long-term capital inflows (primarily from abroad) in order to pick up speed once again.

10 January 2024, © Goldberg & Goldberg für boerse-frankfurt.de

Your opinion counts: Market expectations of investors

All interested investors are invited to participate. It takes only 15 seconds. Every Tuesday you will receive an e-mail with a survey link. You will receive the results of the analysis by e-mail.

Sentiment-Analyse jetzt auch als Podcast

Sie können sich die Sentiment-Analyse direkt über diese Seite anhören oder herunterladen. Es gibt sie natürlich auch auf den üblichen Podcast-Plattformen Spotify, iTunes, Podcaster, Amazon, Google, auf denen Sie ihn abonnieren können.

Sentiment-Index of institutional Investors

| Bullish | Bearish | Neutral | |

| Total | 33% | 44% | 23% |

To previous week | +12% | -12% | unchg. |

DAX (change to previous week): 16.700 (-50 to previous week)

Börse Frankfurt Sentiment Index of institutional investors: -11 points (+24 to previous week)

Sentiment-Index of private Investors

| Bullish | Bearish | Neutral | |

| Total | 34% | 41% | 25% |

To previous week | -10% | +1% | +9% |

DAX (change to previous week): 16.700 (-50 to previous week)

Börse Frankfurt Sentiment Index private investors: -7 points (-11 to previous week)

About the Börse Frankfurt Sentiment Index

The Börse Frankfurt Sentiment Index ranges between -100 (total pessimism) and +100 (total optimism), the transition from positive to negative values marks the neutral line.

More articles from this columnist

| Time | Title |

|---|